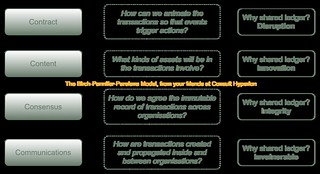

I know, I know, they're not smart and they're not contracts. But in the well-known Birch-Pannifer-Parulava model for thinking about shared ledgers from a business perspective (a model that continues to be refined, even as I type), we've stuck with the term "contract" on our 4C layer, more for marketing reasons that anything else (clients like the "4C" model and find it easy to remember).

So I’m happy to continue to use the word contract But it does bother people, and I think we need to discuss it.

I think folks know this and that’s why there’s been a subtle effort lately to avoid “contract” and “smart contract” in favor of more use-specific labels like “Distributed Application” or “DAO.”

I did have an effort to introduce the new term LAPPS (i.e., Ledger APPlicationS) so as to have a simple and natural term, but it doesn't seem have gained much traction. I suppose the whole "smart contract" thing has just become too embedded. But I agree with the author, and others, that it's time to pick up the cudgels and fight a rearguard action before it is too late.

This is probably a good idea. Calling something that is really just an application a ‘contract’ or ‘smart contract’ sends signals you may not want to send. You don’t, for example, want users of your Hello World app to think they’re [entering a legal contract]

So. LAPPS it is for the time being.

Comments

Post a Comment