In his new book "Digital Human", Chris Skinner sets out a straightforward vision of the bank of the future. He says (I paraphrase slightly) that the back office is about analytics, the middle office is about APIs and the front office is moving to smart apps on smart devices. Here's the three part model that Chris describe.

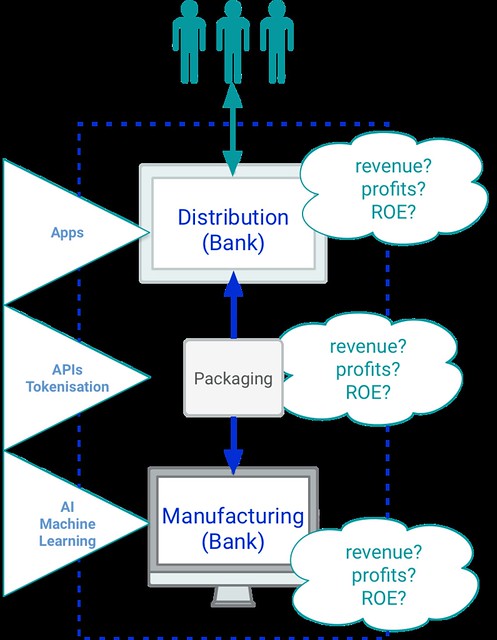

I’ve invented the word “packaging” to describe the additional essential process that is needed to complete what we call the “Amazonisation" of banking, whereby products are manufactured as API services and distributed throughout the consumption of API services. What we don’t know, of course, is how this model will redistribute ROE. How will banks non-banks and neo-banks respond to the split of manufacturing and distribution that the new “packaging” layer (again, not sure if that’s the right term, I just couldn’t think of a better one) brings? That’s obviously a key question and one that is pretty important for organisations who are planning any kind of strategy around financial services in general or payments in particular. Since this includes many of our clients, we spend a lot of time thinking about this and the connection between technological choices that are being made now and the long-term strategic options for organisations.

The Deutsche Bank report is not all doom and gloom though. It goes on to make the point that banks can themselves

Of course, the beneficiaries will be the new financial service providers such as FinTechs or other software suppliers, who can now seamlessly attach their innovative services to the existing (banking) infrastructure. For BigTechs and retailers with a large customer base, the free-of-charge technical interfaces also open up new opportunities with respect to payment services, retail financing or other tailored products. But – somewhat surprisingly, perhaps – individual banks can also benefit. They, too, can act as third-party providers vis-à-vis other account servicing banks and offer an array of new or extended services to their customers, which will intensify competition among all providers.

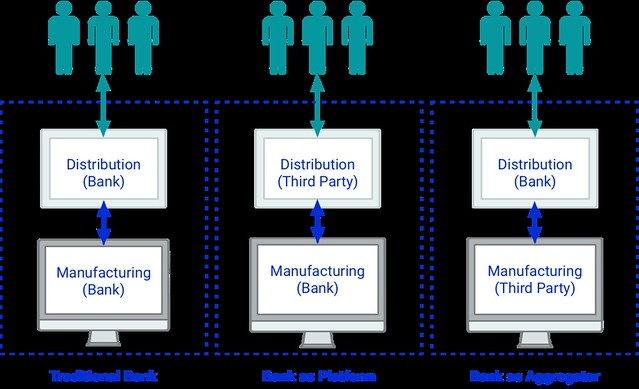

We think it's useful to share them here: the “traditional” bank, the banks as a platform (think Starling) and the bank as an aggregator (think HSBC and Citi).

If, as many people think, it turns out that ROE will remain higher in distribution then the commoditisation of the manufacturing function (as it turns into a “utility”) may well threaten some of the incumbents, because they will not be able to adjust the economics of their manufacturing operation quickly enough to stay in business! This may sound like a radical prediction, but it really is not.

The reality for many banks will, of course, be more of a mixture of these approaches, but you can see the point. The decoupling of the manufacturing and distribution means that banks will have to make some important decisions about where to play, and soon. We’ve already seen how some banks (eg, HSBC) have moved to exploit the aggregator strategy and how some banks (eg, Starling) have moved to become platforms with rich app stores. But what we think may be under-appreciated is the extent to which the traditional bank can develop the packaging process not to shift to one of these strategies but to make itself more efficient and to improve the time-to-market for new products and services while keeping the costs of IT infrastructure under control.

In other words, it makes sense for banks to amazonise themselves.

Comments

Post a Comment